Small business owners who sell business assets may be eligible to contribute the proceeds into superannuation to help fund their retirement.

Benefits

Investing in superannuation boosts your savings to help meet your retirement goals.

The rate of return inside superannuation may be higher after-tax than investing outside superannuation. This is because earnings inside superannuation are taxed at a maximum rate of just 15%, whereas earnings from non-superannuation investments are generally taxed at your marginal tax rate. This helps your savings to grow faster.

Your tax-free component will increase. This amount can be withdrawn tax-free at any age and is also tax-free if paid to a non-tax dependent (such as an adult child) after your death.

How it works

Rather than saving for retirement during their working lives, many small business owners instead use surplus funds to grow their business. The CGT cap exists to allow small business owners to make large contributions into super once business assets have been sold.

To be eligible to use the CGT cap, you must first be eligible for a small business CGT tax concession.

Qualifying for the small business CGT tax concessions

To be eligible for the small business CGT tax concessions, the following basic conditions must be met:

The net value of assets owned by your business and related entities is less than $6 million, or the (aggregated) turnover of the business is less than $2 million each year.

The asset being sold has been used in running a business or it is held ready to be used in running a business (ie is an active asset).

If the asset being sold is a share in a company or an interest in a trust, there must be a ‘significant individual’ and the entity claiming the concession must be a ‘CGT concession stakeholder’ of the company or trust.

If you meet the basic conditions, you are automatically eligible for the 50% active asset reduction which enables you to reduce the capital gain from the sale of a small business active asset by 50%. It is not compulsory to use claim this concession, and in fact, it can sometimes be beneficial not to claim it as it can reduce the amount that can be contributed into superannuation using the CGT cap.

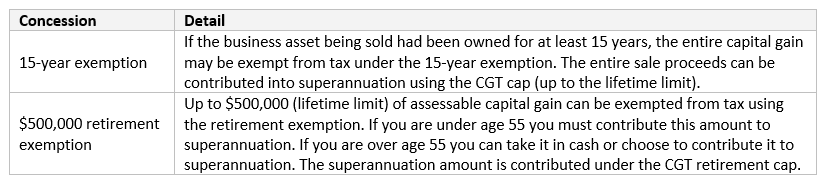

The following table outlines other CGT tax concessions which are available but which have further eligibility conditions attached.

Contributing the proceeds into super

The amount you can contribute into super is limited by contribution caps. The CGT cap enables small business owners who are eligible for CGT tax concessions to contribute larger amounts into super closer to retirement.

The CGT cap provides a lifetime limit of $1.480 million for 2018/19 (the cap is indexed). The $1.480 million limit applies to total contributions made from the following amounts:

up to $500,000 of capital gains which have been exempted using the $500,000 retirement exemption

the sale proceeds from an asset that is eligible for the 15-year exemption

an asset that would otherwise qualify for the concessions but is a pre-CGT asset (purchased before 20 September 1985) or was sold for a capital loss.

To use the CGT cap, you need to make the contribution by the later of the date you lodge your tax return or 30 days after receiving sale proceeds. At the time of making the contribution you need to complete a ‘Capital Gains Tax election form’ and give it to the superannuation fund.

Consequences

As the CGT cap is a lifetime limit, in some cases it may be beneficial to use the non-concessional contribution cap first and retain the CGT cap for future use.

The eligibility criteria for the small business CGT concessions are complex and you must seek tax advice to determine your eligibility.

Time limits apply to be eligible to use the small business CGT concessions and the CGT cap.

If you exceed your CGT cap, the excess contributions will count towards your non-concessional contribution cap.

All contributions to superannuation are preserved until you meet a condition of release.

Fees may be charged for your superannuation contributions. You should check the details in the fee section of your Statement of Advice and the Product Disclosure Statement (PDS) for your superannuation fund.

Date: 1 July 2018